Written by

Published May 2026

Summary

- Funding gives SMEs the stability to manage cash flow and the flexibility to invest in growth.

- A strong business credit score, healthy financial records, and a clear funding plan can improve your chances of success.

- Loans offer flexibility, but they cost more over time. Grants do not need repaying, but they are harder to secure and use.

- Alternative funding options, such as asset finance, invoice finance, and equity finance, can suit businesses that do not fit traditional loan or grant routes.

Why funding matters

For most small businesses, funding is essential. Beyond sustaining operations or providing cash flow stability, access to capital allows SMEs to remain resilient, flexible, and innovative. It’s also pivotal in helping companies grow, expand, and invest in every operational area, from equipment and research to teams and culture.

SMEs account for 99.9% of all UK businesses, making their success foundational to the wider economy. Whether creating opportunities or pioneering innovation, small businesses keep industries moving both here on home ground and overseas. And funding helps make this happen.

Key takeaway

Funding gives SMEs the stability to manage cash flow and the flexibility to invest in growth.

Things to think about when applying

Your business credit score

When thinking about funding, investment, loans, or acquiring other financial products, the best place to start is with your business credit score. This will be pivotal in unlocking key areas of funding, as well as agreeing more flexible credit terms, so ensuring your business credit score is the best it can be – and improving it if not – is essential.

Your company’s financial health

Lenders will want the full details of your financials, so you should have at least 12 months of bank statements, accounts, and balance sheets to hand. Being able to show a positive and stable cash flow and prove tax compliance will also put you in a positive light.

Your strengths and reason ‘why’

Why your industry, team, business…and why now? Explaining all of this can give you a competitive edge over others looking to secure the same funding. A compelling narrative and plan can be attractive to investors in particular, show that you’re a lower risk, and even score you more flexible credit terms.

What you plan to do with the funding

It’s extremely unlikely you’ll be given any type of funding with no questions asked. Lenders and those in charge of giving grants will need to know that the money is being put to good use and will generate results. Defining a clear purpose for the funding, alongside a growth plan and projections (of both your business and the wider industry), will better help your chances of securing finance.

Key takeaway

A strong business credit score, healthy financial records, and a clear funding plan can improve your chances of success.

What’s the difference between loans and grants?

Loans

A loan is one of the most common funding methods available, giving you capital to invest, grow, or manage cash flow. You’ll need to pay the loan back, alongside interest, according to pre-agreed terms.

Common loan types include:

- Secured, which often allows you to borrow higher amounts. However, this will need to be backed by an asset, like a home or car, to serve as collateral in case you fail to make repayments.

- Unsecured, which doesn’t require an asset for collateral. Instead you can get faster access to funding but are likely to have a lower borrowing limit and higher interest rate.

- Government-backed, which means the loans are guaranteed by the government and are therefore less risky for lenders and more accessible for borrowers.

- Bridging, which is a short-term, secured loan that aims to help SMEs ‘bridge the gap’ between purchases or payments. They can be secured quickly, but often come with higher interest rates.

Pros

- You don’t need to have immediate profits for your business to grow, buy assets, or improve cash flow.

- Loans can be used for a wide range of business reasons, with less rules around what you can and can’t do with it.

- Fixed repayments ensure you can budget appropriately and accurately.

- You can actually improve your company’s credit score through timely repayments.

Cons

- Interest rates and fees can vary massively depending on your loan agreement.

- Depending on the loan, there may be strict criteria for application.

- Fixed repayments will be required even during periods of low revenue, which could be damaging to your cash flow.

- A lender may require a guarantee or collateral which makes you personally liable for repayments and could mean you risk losing assets.

Grants

Grants can be thought of as ‘free money’ and are a fixed-sum typically awarded to small businesses by the government, local authorities, enterprise agencies, charities and non-profit organisations, or support programmes.

The main difference between a grant and a loan is that you won’t need to pay a grant back. Think of it as a helping hand, designed to boost your SME with a specific project or in certain business areas.

Common grants include:

- Employment and training, to encourage skills and employability, particularly in a specific geographic location or industry.

- Industry or sector specific, to boost growth across a range of topics and areas, such as sustainability or the arts.

- Innovation and research, to support the development of new products and services, particularly in areas that the UK may be lacking.

- Regional development, to help encourage economic, employment, and infrastructure growth.

Pros

- You won’t need to pay the grant back.

- They can help with cash flow for a specific area of your business, like research and development, meaning your day-to-day operations don’t have to stop.

- Receiving a grant can come with a lot of publicity, which means free PR for your business.

- The UK has a lot of different grants available, for a wide range of areas, projects, and topics.

Cons

- There may be conditions or parameters on how you use the money.

- There may be a time limit in which you must complete certain tasks, such as undertaking and publishing research.

- Competition can be high, and creating a show-stopping application can be heavy on your time, effort, and resources.

- You and your team may be required to undertake training before you’re granted the funds. Again, it can be a time-heavy venture.

- You may need to match the amount of money being granted, which could immediately rule some SMEs out.

Key takeaway

Loans offer flexibility, but they cost more over time. Grants do not need repaying, but they are harder to secure and use.

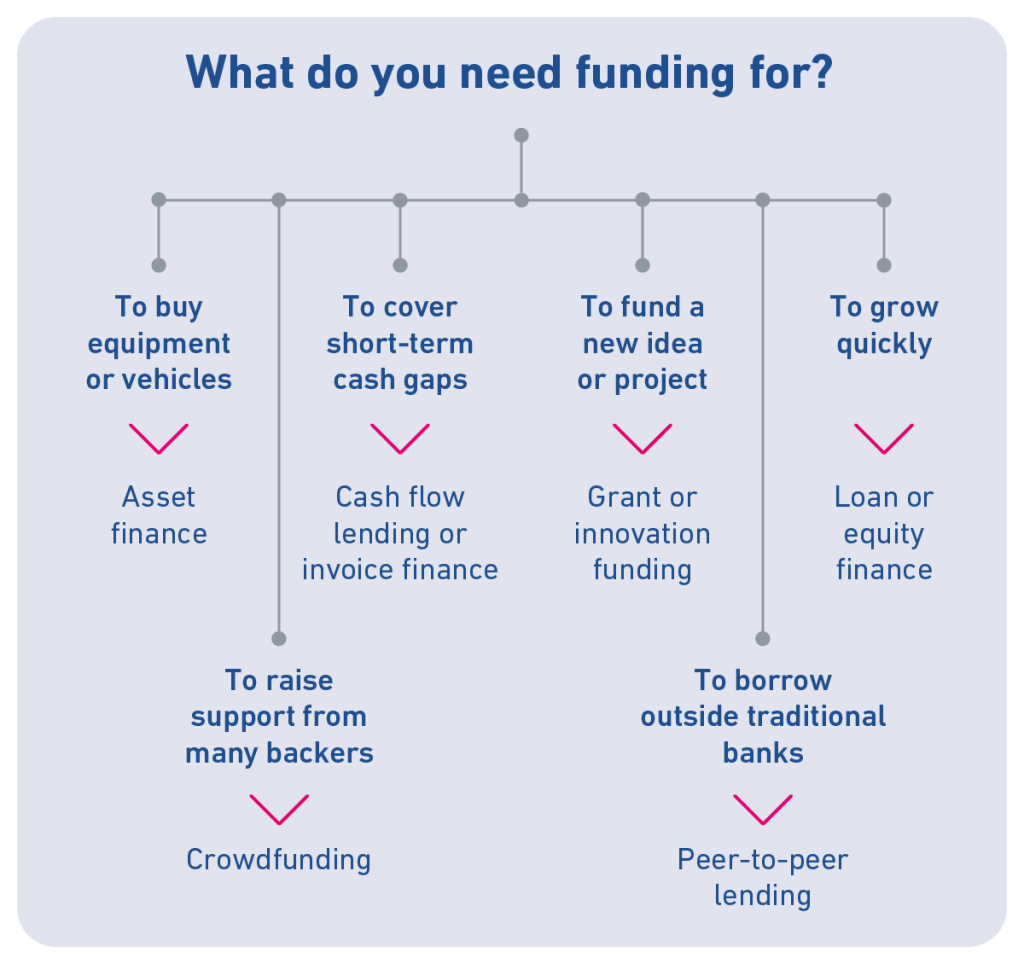

Alternative funding to consider

They may be the most common, but loans and grants aren’t your only funding options. Take a look at the other – sometimes less conventional – ways you can inject capital into your business.

Asset finance

This is typically used when your business needs to purchase vehicles, machinery, tools, or equipment. The asset itself can be used as collateral and you can often spread the cost of the item through hire-purchase or leasing.

Cash flow lending

Cash flow lenders look at your ability to repay a loan based on your cash flow and projected revenue, instead of relying on physical assets as collateral. There is usually a higher risk attached to this type of lending so it’s likely to involve higher interest rates too.

Crowd funding

This means to raise smaller amounts of funding from a larger number of people. Typically done via online platforms, the return for crowd funding investors can be rewards, interest, or even equity in your business.

Equity finance

A popular choice for startups, equity financing involves selling a portion of your company’s shares to investors. They will then have a stake in the business’ future growth. This type of lending can be risky for investors, so a solid business and growth plan will be essential.

Invoice financing

This is a way to bridge the gap between sending an invoice and receiving payment for it. It involves borrowing money against the value of your outstanding customer invoices which, if you have reliable customers, can be a great option.

Peer-to-peer (P2P) lending

This is another method of lending facilitated by online platforms. It links companies with private investors directly, bypassing traditional banks. These online platforms can help investors find the right company to provide capital for by matching them to things like risk level, meaning there’s lending opportunities for every type of SME.

Key takeaway

Alternative funding options, such as asset finance, invoice finance, and equity finance, can suit businesses that do not fit traditional loan or grant routes.

Where to find funding

Finding funding can be a time-consuming activity. Depending on the type you’re looking for, you may wish to look for investors online, using P2P or crowdfunding platforms. Alternatively, the process could be as simple as approaching one of the major banks or a conventional commercial lender.

Central and local governments are a great place to check, as they will have a directory of both government-backed and independent finance and support schemes. You’ll also find non-profits, foundations, and corporations here, all of which have funding available.

Being active in your industry’s community through growth hubs, programmes, and associations is a great way to get information about different types of funding. This is particularly handy for grants and anything related to startup funding. You can also often get advice on applications and insight on the likelihood of success.

Alternatively, leaning on your company’s USPs can open up specialist support, such as funding from The King’s Trust. While this one is specifically for startups and younger entrepreneurs, there will likely be a funding group that aligns with your SME’s unique offering.

We can help

We provide tools and solutions to help small business owners make better decisions about their suppliers and customers, and understand and manage their own business credit score.

- Experian Business Express allows you to run credit checks and monitor any company you work with, so you can spot signs of trouble early on and make informed decisions.

- With My Business Profile, you get full visibility of your business credit profile, enabling you to understand what’s affecting your company credit score and preventing you from being able to obtain that all important company finance.

- With our Score Review Service, simply provide additional financial information to us and we’ll review your business credit report. 96% of reviews result in a positive uplift.

Get in touch

Make your business stronger. Review your own business credit score and improve it.

Contact us