Consumer Duty regulation – what does it mean for credit risk?

Who needs to prepare for the Consumer Duty regulation?

Preparation is well underway for those in the banking and financial services sectors. Whilst clarity is emerging for what the regulation means for product teams, compliance, and customer services, how are credit risk teams preparing and what are the key focus areas?

Whilst there is plenty of guidance on the Consumer Duty regulation and what it means for banks and financial services, the requirements for credit risk professionals in particular continue to come under discussion. In this blog, we talk through what credit risk and collections teams are doing to prepare for the duty, and the emerging areas of focus.

What is the Consumer Duty regulation?

The Financial Conduct Authority (FCA) published the Consumer Duty rules and final guidance on 27th July 2022 after a year of consultation1. The Consumer Duty is a key element of the FCA’s 3-year plan and sets a higher bar for financial services firms to ensure they pro-actively work to deliver good customer outcomes at all stages of the customer journey and lifecycle.

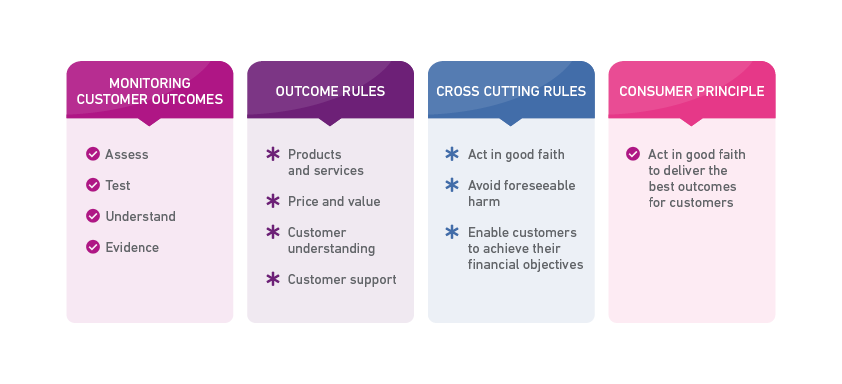

The Consumer Duty is comprised of 3 cross cutting rules and 4 outcome rules:

What’s happened since the rules were published?

The FCA has recently published its findings2 of the multi-firm review of implementation plans and found that whilst there is good evidence of firms embracing the necessary changes and mobilising effectively, there were some examples where firms were expected to do more to meet the requirements of Consumer Duty.

- Some firms need to ensure that they have effectively prioritised their activities to address areas where they are furthest away from the requirements.

- A re-emphasis on the need to ensure that the substantive requirements of the duty are being considered and not being only superficially considered.

- Effective engagement with 3rd parties involved in the distribution chain, ensuring that plans were clear on what information is shared and how this is implemented.

What are Banks and Financial Services focusing on for Consumer Duty?

Our engagement has already revealed a number of areas where firms are reviewing current practices and processes to see what might be required to meet the requirements of the Duty. These include:

- Data quality: The FCA frequently refers to accuracy and quality of information used by firms to inform your engagement with customers. Access to good quality data is essential to informing one of the Duty’s four core outcomes, notably Customer Understanding; but it also informs the other outcomes including optimising Product Performance, informing Price and Value and improving the quality of your Customer Support. Maintaining an accurate view of your customers, their contact details and channel preferences is essential to communicate effectively. Maintenance of an individual’s credit history and the sharing of timely and accurate information with credit bureau is also seen as important to minimise detriment to consumers and their use of credit

- Vulnerability: This is a clear focus area as firms look to enhance their identification and support for consumers who show signs of both financial and non-financial vulnerability. This is perceived as one of the biggest gaps regulated firms have today and therefore where most focus is placed. A key challenge is capturing signs of vulnerability across all customer touchpoints and having appropriate responses and activities to tailor communications and customer decisions.

- Affordability: Ensuring consumers receive tailored support needed when in, or at risk of financial difficulty. A lot of focus has been placed on enhancing affordability assessments at onboarding in recent years, but with the “Avoid Foreseeable Harm” cross cutting rule, firms need to ensure the same discipline is applied across the entire customer lifecycle and at all key decision points.

Looking to implementation, we have also observed the following trends:

- Workstreams: A common approach to Consumer Duty activity is into split workstreams by each of the cross-cutting or outcome rules, with cross-business teams contributing. This approach helps ensure all compliance considerations are considered. But firms need to ensure that this joins up to demonstrate adherence to the substantive requirements of the new duty. This requires a multi-disciplinary approach, involving teams from across a business including, Marketing, Product, Analytics, Data and Customer Support. Seeing this simply as a Compliance exercise, ignores the opportunity that Consumer Duty provides to create competitive advantage by improving how you acquire and manage customers.

- Increasing knowledge: Knowledge levels and activity is on the rise as Consumer Duty regulation and business change activities are rolled out across organisations and the 31st July 2023 deadline gets ever closer. We expect this to further increase as the internal communications and roll-out plans become more visible within organisations.

- Working with intermediaries: The Duty puts a new emphasis on how firms interact with intermediaries including Brokers, Dealers and Price Comparison websites. UK credit bureaux are also an integral part of this ecosystem, and we’ve already started sharing information and our response to the Duty and the role that our products and services place in supporting firms in their engagement with consumers. Working collaboratively to improve consumer outcomes is the collective objective that everyone needs to focus on.

What are main focus areas and approaches being taken?

With the backdrop of macro-economic instability and a cost-of-living crisis, the FCA have regularly communicated their expectations of firms to support their customers during these challenging times3. This, alongside the recently published findings of the FCA’s implementation plan review, is dictating the priorities of many firms.

The areas of focus which indicate the biggest gap to Consumer Duty compliance align closely with the key themes of regulation in recent years such as ensuring robust affordability assessments, providing tailored support to customers in financial difficulty or with signs of vulnerability and ensuring that consumers understand the products they are purchasing and can interact effectively with firms. Let’s review these topics in more detail.

Demonstrating good customer outcomes

The focus is shifting towards evidencing affordability outcomes with the tasks of defining outcomes and how to monitor these being at the forefront of activity. To demonstrate good customer outcomes many firms are looking to enhance their affordability strategy to monitor changes throughout the customer lifecycle and not only limit these to originations decisions and collections events. In particular, firms with little insight on the ongoing customer affordability position of their lending portfolios are now looking to use credit bureau data to solve this blind spot and increase their understanding of a customer’s financial resilience. This is often a new need for fixed term products where traditionally the wider financial position of customers has not been regularly updated and reviewed.

Consumer Support / Vulnerability

There is an increasing requirement to identify customers who are in financial difficulty and ensure that tailored support is provided. Firms are therefore looking to enhance their pre-delinquency capabilities, both in terms of identification of at-risk consumers and how they engage and offer customers tailored support via appropriate communication channels. As an example, lenders are seeking better sources of expenditure date so that they can identify changes in energy payments or mortgage payments and engage those customers with an increased risk of entering financial difficulty.

Another key challenge is gaining sufficient customer engagement where timely and personalised communications provide the best customer response. Simplified or blanket communication approaches are unlikely to get the desired outcomes, therefore a test and learn approach is required to ensure customers react positively and engage appropriately. The collection and actioning of information on a customer’s non-financial vulnerability is also seen of importance in evidencing how firms are ensuring that services are fair and accessible for all. Data such as physical disabilities and support needs can be used to improve customer experiences to demonstrate fairer access to finance. We’re seeing a renewed urgency from firms to work collaboratively with consumers to share information so that services can be better targeted and tailored to meet the needs of vulnerable customers.

Product Design & Target Market

The product and services outcome requires firms to review their products and ensure that these meet the needs and objectives of the target market. This requires firms to identify the target market and regularly review to ensure that the needs are continuing to be met. Lenders are increasingly looking to market level data to deliver a data-led approach to meeting this need through assessment of market size and consumer segments and analysing their use of credit and repayment performance.

Alongside this firms must ensure that their distribution strategy is designed to deliver products to the relevant target market and, where sold outside of the target market, that this doesn’t cause poor customer outcomes. Firms need to consider the data available to support this requirement and whether broader data sources covering consumer demographics and behaviour can supplement internal data sources. These data sources can be used to identify and mitigate the risk of unintended bias in product design such as new credit scores, without the risk of compromising performance. This can be used to evidence a commitment to fairness in the development of and implementation of new products.

Monitoring

As touched on in product design there are new monitoring requirements brought about by Consumer Duty to ensure that the requirement to regularly review and measure customer outcomes is being met, with it highly unlikely that existing MI and data sources will be sufficient to meet this need. Firms need to ensure that any new MI or reporting measures consumer outcomes across multiple customer touchpoints and that the insight allows clear identification where consumer duty rules are not being fully met. Some lenders have started building enhanced monitoring of consumer behaviour with a focus on financial and behaviour impacts wider than the lender/customer relationship. This helps demonstrate performance against the “foreseeable harm” and “achieving financial objectives” cross-cutting rules.

How can we support your preparation for Consumer Duty?

We already support many organisations with data and services to ensure good customer outcomes are achieved. This extends beyond banking and financial services, into the other areas touched by Consumer Duty including Insurance, Telecoms and specialist Asset Finance and Auto lending markets.

A new service is being trialled to allow firms to benchmark customer outcomes against relevant markets and peer groups and it is expected this information can support firms’ Consumer Duty monitoring and benchmarking requirements. This will touch on some of the key issues of data quality, as well as compliant resolution to provide you with metrics that can be used to benchmark, audit and evidence your response to the Duty and improvements that may be being made in your organisation.

Get in touch

Speak with one of our consulting team about this capability or Consumer Duty regulation.

Let's talkFurther reading

How Plata used Experian’s Work Report to increase loan conversions

Discover how Plata increased loan conversions using Experian Work Report™, accessing payroll-verified income data to reduce friction and improve lending decisions

Fraud Index Report: Q1 2026

How has fraud changed over the past year? Read the latest fraud statistics and trends in Experian's Fraud Index Report for Q1 2026.

Senior Managers and Certification Regime: What You Need

SMCR essentials, governance and compliance explained in simple terms. Learn what it is, what’s required and how to keep your business secure.

Data that delivers: Four takeaways from the AI and Big Data Expo

Explore four key takeaways from the AI & Big Data Expo, revealing why data quality, governance and ethics are essential foundations for scaling AI successfully.

The Economic Crime and Corporate Transparency Act

The Economic Crime & Corporate Transparency Act is revolutionising how we fight must fraud and FinCrime. Understand why and your company’s risk.

A guide to background checks in financial services, banking and fintech

Make safer hires in banking & FS. Discover the checks that reduce fraud, avoid fines, and protect your business from hidden risks and reputational harm.

How Open Banking is reshaping mortgage lending at Leeds Building Society

We aim to help lenders drive automation, speed up decisions, and support financial inclusion in mortgage lending, giving consumers more control and support.

Empowering customers: The role of Support Hub in enhancing NewDay’s services

Hear from NewDay, and how they are supporting their vulnerable customers and what they're doing to empower call centre staff.

Affordability assessments for insurers: Why you need this essential risk management function

We explore why premiums are risk, how consumers are impacted, and why insurers need to understand customer affordability.

- Consumer Duty, Financial Conduct Authority

- Consumer Duty implementation plans, Financial Conduct Authority

- FCA tells lenders to support consumers struggling with the cost of living, Financial Conduct Authority