Summary

- A low business credit score can limit access to finance, lead to higher costs and affect how suppliers and partners assess your risk.

- Common drivers include late payments, high debt levels, legal actions and frequent credit applications, with payment behaviour now carrying greater weight.

- Reviewing your credit profile helps you identify issues, correct inaccuracies and improve your position before applying for finance.

Running a business means making decisions that affect cash flow, investment and growth. Your business credit score plays a direct role in how those decisions play out. If your score is low, it can restrict access to finance, affect payment terms with suppliers and influence how other businesses assess risk when deciding whether to work with you.

If you have been refused credit or offered less favourable terms, your business credit score is likely part of the reason.

What is a poor business credit score?

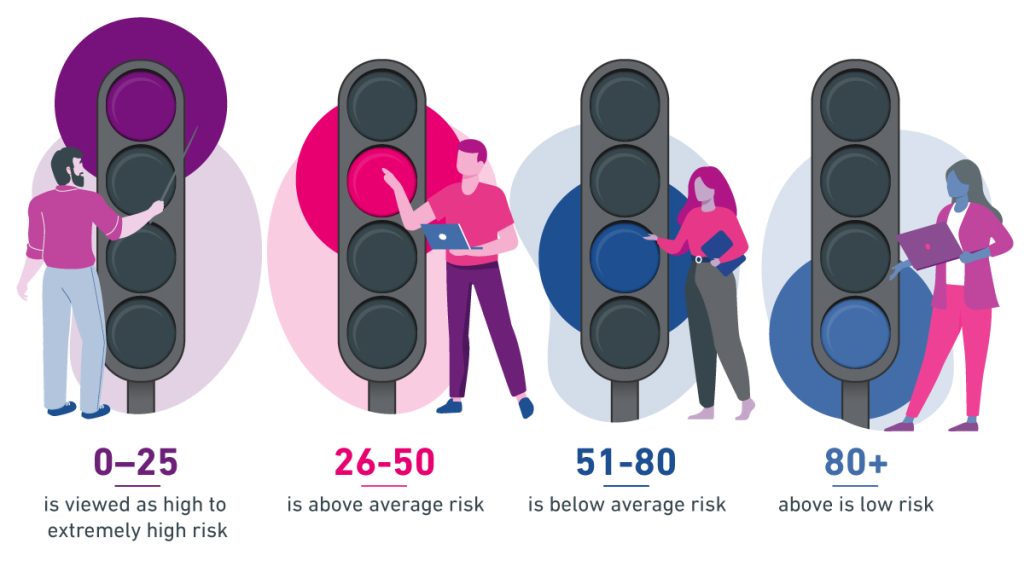

There is no universal cut off between a good and poor business credit score. In the UK, our business credit scores typically run on a 0 to 100 scale, where lower scores indicate higher risk.

As a general benchmark:

- 0 – 25 is viewed as high to extremely high risk

- 26 – 50 is above average risk

- 51 – 80 is below average risk

- 81 and above is low risk

A lower score does not automatically mean finance will be declined, but it often leads to closer scrutiny, higher costs or tighter terms.

What’s impacting your score?

There are several factors that can negatively affect your business credit report. Common examples include:

Missed or late payments on loans, credit cards or trade credit

County Court Judgments (CCJs) or other legal action

Bankruptcy or other insolvency events

Filing accounts late with Companies House

High levels of outstanding debt

Making multiple credit applications at the same time

Payment behaviour and filing history now carry greater weight than they did previously. Repeated minor delays can have a measurable impact.

Seeing what lenders see

Reviewing your business credit profile gives you clarity on how your business is assessed and why decisions are made. It allows you to:

- Understand which factors are pulling your score down

- Identify incorrect or outdated information

- Monitor changes as your financial position improves

This visibility puts you in a stronger position when applying for credit or negotiating terms, rather than reacting after a decision has already been made.

A poor business credit score rarely comes down to a single problem. It reflects how consistently your business meets its financial obligations and how accurately that activity is reported.

Keeping track of your business credit profile helps you spot issues early, reduce unnecessary risk and protect your ability to access finance when it matters.

How we can help

If you’re thinking about applying for a business loan, or are in the middle of doing so, and would like to give your credit score a health check, we can help.

My Business Profile can give you the top five factors influencing your business credit score, to help give you the best chance of success when applying for business credit.

View your business credit score or speak to one of our experts.

View your business credit score

See your Experian Business Credit Score for free with My Business Profile

Let's go