Banks and Financial Institutions are, by now, well versed in submissions to both national regulators and the European Central Bank (ECB). However, the launch of the Anacredit regulation, brings a new dawn in the level of granularity needed for regulatory submissions.

What is the Anacredit regulation?

In a nutshell, Anacredit is applicable to all institutions which have more than €25,000 credit risk exposure to a counterparty. The institution is obliged to report 106 attributes for each of the exposures. No other regulation from the ECB has mandated such a granular level of data requirement by financial institutions.

Why do we need this regulation?

This regulation is brought about on the back of the financial crisis when the central banks were unable to model various credit risk scenarios to understand financial stability and to perform economic research on a granular level. Anacredit will make it possible to identify, aggregate and compare credit exposures on a loan by loan basis.

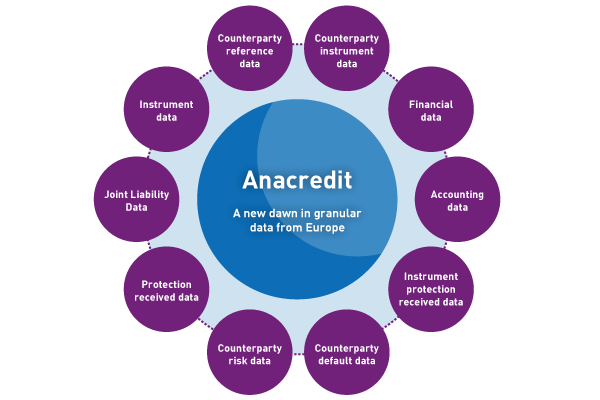

What data attributes are required?

There are 106 data attributes required from the financial institutions. The infographic below shows the high-level data types, each of which have further attributes within it.

When do you need to submit the data?

The final go-live date for submissions to the ECB is September 2018. However, submissions will be made by national regulators to the ECB, rather than from the Financial Institutions to the ECB.

This forces organisations to have an earlier deadline for submissions. Every regulator has their own deadline for submissions of Anacredit data to them. For example, Germany’s Bundesbank has stipulated a different timeline which comprises of test submissions, production pilot and production data submissions which begins from December 2017.

How should this data be submitted?

This data is likely to be submitted to the various regulators in the format of an xml feed at various frequencies, some monthly and some quarterly. Also, there is an ongoing legal interpretation issue on when the changes to counterparty data should be submitted.

What are the key challenges faced by Financial Institutions?

1) Data Sourcing:

Some of the data items that the ECB has requested are not available that easily in the same way that other counterparty data is available. For example, number of employees or balance sheet size. These are not common Know Your Customer (KYC) questions that every institution asks when they onboard a client. Also, there is no automated way of monitoring the changes in employee count or balance sheet size.

2) Data Ownership:

In the majority of firms, the data ownership is still a nascent concept and they are slow in the process of identification of data owners and assigning roles and responsibilities. The data sets requested by Anacredit are owned by multiple business functions within the organisation which makes the ownership discussion very challenging.

3) Data Governance process:

Within organisations, Data Governance is not mature enough to onboard the Anacredit data items as critical or key data elements. This means the usual governance process on data items which are critical may not apply. For example, the measuring and monitoring of data quality on all 106 attributes is challenging. For some of the data items, it is extremely difficult to codify data quality rules.

4) Technology integration

Traditionally, some of the reference data elements and risk data were never fed to regulatory reporting platforms. These are held in a separate data warehouse or data mart with no piping and plumbing to a finance data warehouse. It is a lot of effort for an organisation to integrate various systems into a common reporting platform.

How can Experian help?

Having worked with Experian’s data management tool, I am confident it can help prepare your data for meeting compliance obligations, including Anacredit.

Experian’s tools have many useful features to help you prepare your data; here are just a few:

- Sourcing data from multiple data warehouses or data marts

- Performing both single layer and multilayer data quality checks

- Producing Data Quality Dashboards

- Transforming data to meet the strict validation requirements as requested by the ECB

- Extracting the data into a format that is required for downstream use by Regulatory reporting applications

If you’d like to learn more about Experian’s data mangement tools, you can download the brochure, try the free data profiler version, or book a demo today.

The views in this blog are the opinion of the writer, not Experian Data Quality.