Furthermore, the effects of Brexit and what this will mean for your business in the long-term still needs testing to try and better understand how the UK, Europe and the US will work together in the future.

Our research shows that many firms are struggling to react fast enough in these difficult times and adapt their scenario models to the changes caused by the pandemic. Others are finding it difficult to tap into models sufficiently reflective of the true quality of their own portfolios.

Stress testing your portfolios

Alongside scenario modelling, stress testing is vital for you to understand the sensitivities and vulnerabilities within your portfolio. The rate of change across a number of factors is relentless, from economic challenges, such as the one being caused by COVID-19, to the introduction or emergence of new technologies, businesses need to prepare for a wide variety of potential situations.

Currently, your stress tests will be based on scenarios before the pandemic struck and the sheer scale of the pandemic has moved lenders into uncharted waters, and you’ll now need to rapidly calibrate the outer limits of possible actions with new data. In fact, today’s challenges call for stress tests that can quickly adjust to changing economic scenarios, different business mixes and evolving risk profiles. Effectively re-engineered, they can help you mitigate risk, identify valuable avenues for growth and better protect your credit portfolio. Left in their pre-pandemic form, they’ll probably tell you entirely the wrong story.

IFRS 9 – forward looking credit loss modelling

Created to measure and report financial assets and liabilities, the international financial reporting standard IFRS 9 can be an incredibly powerful tool in understanding risk and meeting your regulatory responsibilities. However, like so many tools trusted by the financial industry, it needs to be recalibrated if it’s to provide accurate, relevant insights in the light of COVID-19.

Even before the crisis began, there was evidence that the IFRS 9 models some firms were using just weren’t strong enough to deliver the accuracy needed. Some only factored in economics at macro level, while others weren’t sensitive enough to specific portfolio shape or quality, changing risk profiles or the need to make quick, easy management overlays. The pandemic has brought these shortfalls into sharp focus and presents the industry with an opportunity to address these weaknesses while adjusting for a post-pandemic world.

How can Experian support model updates and testing?

World-class economic scenario modelling

Since the pandemic began, our internationally renowned economic forecasters and modellers have been building robust, evidenced scenarios that map the likely impact of the crisis on the UK economy, including critical factors

such as unemployment, inflation, credit availability and sterling depreciation. Each scenario is based on the Government views which follow the recommendations set out for managing the epidemic.

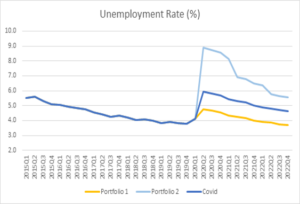

Each sees a sharp rise in unemployment in quarter two of 2020, which is likely to cause major income shock for British consumers. The scenarios show us that the greater the income shock and the deeper the fall in sterling, the more dramatic and drawn-out the economic implications for the UK will be, including worsening credit availability, rising inflation and longer, deeper levels of unemployment, that impact the financial security of consumers – as well as the stability of portfolios. Building an in-depth understanding of the implications of various likely scenarios is fundamental to stabilising and protecting portfolios as firms move forward.

Portfolio-tailored unemployment curves

Protecting your firm begins with building a clear picture of the specific risks you face, which is why we offer a unique solution to understanding estimated unemployment within your portfolio. By combining our market leading forecasting with CAIS data, we can map probable unemployment curves against COVID-19 economic scenarios, tailored directly to the customers you serve.

We’ve developed this capability through rigorous, extensive research, and each of the scenarios we create is stochastically modelled to make sure it remains unbiased and objective. The PRA (Prudential Regulatory Authority) advises that scenario modelling should always be reasonable, robust and supportable, and that’s been fundamental to our approach.

IFRS 9 Tailored Solution Suite

This agile Experian product suite helps you address your specific IFRS 9 challenges, including data, reports, software and modelling. Experian can meet your IFRS9 modelling requirements with our traditional audit proven bespoke solutions. We can combine our extensive CAIS data coverage, with our industry leading probability weighted economic scenario forecasts, with your internal view of your portfolio to suit your requirements providing all the elements of expected credit loss forecasting under IFRS 9 and helping you move confidently forward.

Our approach explicitly builds the relationship between the performance of each segment of your portfolio and the changes we’re seeing in the economy, improving accuracy and aligning with your risk appetite.

IFRS 9 Credit Loss Insight

Experian are developing a powerful, flexible, on-demand software tool that calculates Expected Credit Loss (ECL) forecasts in just a few clicks – IFRS 9 Credit Loss Insight (ICLI). Based on CAIS data and industry-leading, forward-looking, probability weighted scenarios, it enables you to quickly generate and evaluate your own ECL models. Models can be generated automatically or you can control the shape and content of the models. We ensure the underlying data and scenarios are kept up to date, giving you the confidence that your calculations are timely and accurate.

Experian is here to help. We know that for many firms, credit portfolios will be fluctuating, evolving and showing signs of stress. We also know that having the resources in house to understand those changes, identify patterns and create new strategies may be unrealistic when teams are depleted, dispersed and dealing with huge new pressures.

If you would like to speak to one of our experts, please contact us or get in touch with your account manager.