The Fraud Index data from 2025 paints a clear picture: application fraud is still evolving and often faster than controls can adapt. While overall application volumes increased by 8% year-on-year, the composition and behaviour of reported fraud cases shifted. Identity based attacks remain the greatest threat, first-party fraud attempts are on the rise across most of the traditional lending-based products.

1. Application volumes are rising

Despite continued challenging economic and global political backdrops, application volumes processed within the data consortia increased in 2025, most notably in Mortgages (+19%), Cards (+14%) and in Motor/Asset Finance (+12.4%), however remain below pre-pandemic levels.

2. Identity fraud dominates

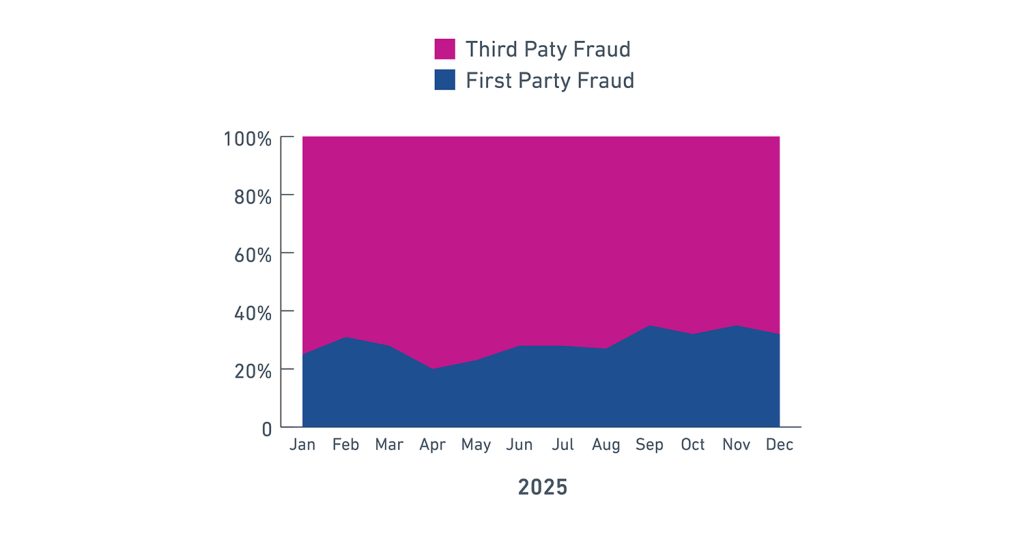

Identity (Third-Party) driven attacks accounted for 71% of all confirmed fraud cases reported.

Within Identity Fraud, the reasons for filing underscore a key industry truth: Identity fraud is overwhelmingly driven by impersonation and synthetic/false identities.

ID Theft – Other is the largest reason at 55% and which is largely synthetic/falsely constructed identities.

Current Address impersonation, once the leading identity reason now accounts for 41% with False Identity documents recorded as the primary fraud reason falling to just 3.8%.

This likely comes as no surprise to many industry professionals, as Fraud-as-a-Service (FaaS) has industrialised identity fraud, leveraging AI to produce high-quality forgeries that are widely accessible. Combine this with deepfake injections and presentation attacks, the fraudsters now attack the ID Verification stage of the digital onboarding journey.

These online “template farms” now offer more than 360,000 templates from over 15,000 issuers¹, allowing criminals to generate convincing identity packages with minimal effort and cost. Even after takedowns, these services quickly reappear on new domains, demonstrating the resilience of the FaaS ecosystem.

3. First-party fraud is still deeply rooted in information misrepresentation

First-Party fraud comprised of 29% of cases in 2025, increasing across most of the traditional lending products in 2025 with the dominant driver being Hidden Adverse History, accounting for 48.2% of reported cases.

Document based misrepresentation, once a staple, accounted for just 6.2% and attributed mostly to mortgage applications whilst “Fronting” remained material in the motor/asset finance vertical (9.3%).

4. Fraud by product: where the pressure really is

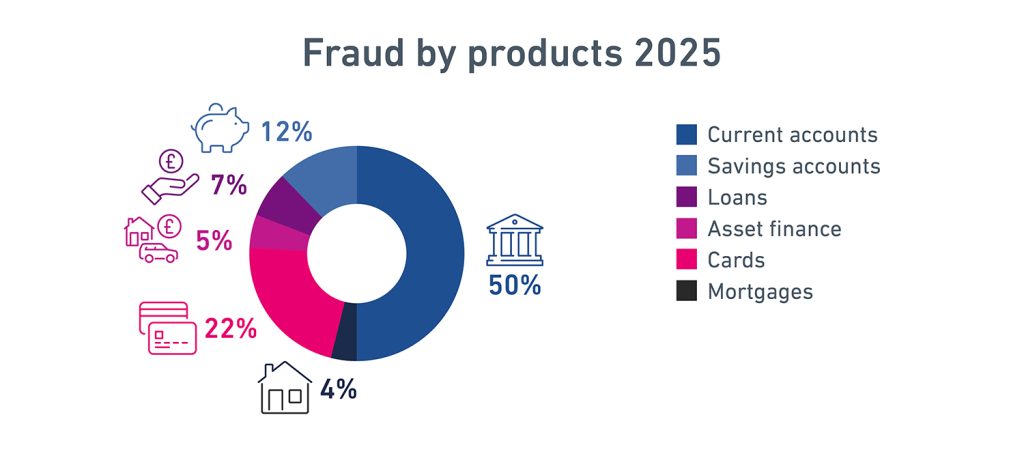

Half of all confirmed fraud cases in 2025 originated from Current Accounts:

When you normalise fraud by application volumes, Current Accounts again stand out with a 1.37% confirmed fraud rate and 2.42% suspect rate.

This reinforces a familiar narrative that Current Accounts remain the primary gateway for fraud ecosystems, from mule activity to payment evasion and synthetic identity anchoring.

5. The hidden story: suspect cases are outpacing confirmed fraud

One of the most operationally significant findings is the ratio of confirmed to suspected fraud (37% confirmed, 63% suspected)

This indicates operational teams may be prioritising efficiency over thorough investigation or strategy teams are prioritising the wrong referrals for them to work. This weakens the overall strength of the data-sharing groups as fewer fraud signals are shared across the network and can create pockets of vulnerability.

For teams prioritising efficiency, optimisations of case prioritisation workflows are just as important as detection itself, with machine learning and automated decisioning able to reduce the noise and allow concentrated effort on high priority cases.

What fraud teams should focus on in 2026

Based on the data, three priorities stand out:

1. Strengthen synthetic/false identity detection

With impersonation and synthetic/false profiles dominating identity fraud, firms should double down on:

- Cross institution link analysis

- Device and behavioural biometrics

- Address level patterning

- Document forensics

- Consortium driven risk scoring

2. Target First Party Hidden Adverse Behaviour

This requires more than document checks. Consider:

- Recency weighted credit trends

- Affordability by behaviour modelling

- Bureau and consortium refresh during underwriting

- Multi signal income estimation

3. Reduce the Suspect Load with Better Decisioning

High suspect volumes drain investigative capacity. Teams should:

- Deploy AI based investigator assistant tools

- Improve machine learning explainability

- Implement consistent QA loops

- Refine alerting thresholds through continuous optimisation and calibration

Final thoughts

The 2025 Fraud Index makes one thing clear: Application fraud is no longer a point in time risk, it’s an ecosystem risk.

With the right data-driven strategies, continued access to cross-lender (consortia) intelligence, and improved in-life fraud monitoring, fraud teams can stay ahead of an increasingly industrialised FaaS adversary. By layering into this mix traditional bureau and affordability based data alongside advanced, AI based analytics, to deliver powerful first party fraud lending models will significantly help to counter the increasing first party fraud risk that has emerged.

How can we help?

As fraud and financial crime increase, it’s more important than ever to deploy a robust, multi-layered approach to preventing it. Get in touch to find out more on how Experian’s Identity and Fraud Solutions can protect your organization.

¹ Source: fintech.global