What is KYC?Support compliance With ‘Know Your Customer’ Checks

Guide

Know Your Customer (KYC) checks play a pivotal role in identifying and mitigating potential risk of fraud and financial crime. Put simply, they’re invaluable for business safety and security, as well as ensuring you remain compliant with the right laws and regulations.

It’s estimated that financial crime costs the UK economy £290 billion annually, with many firms spending up to £100 million on remediation activity individually each year. In an era dominated by digital transactions and evolving financial landscapes, safeguarding against fraud has become a top priority for financial service organisations.

In this guide, we take a look at the various ways you can conduct KYC checks, when to run them, and the benefits they offer.

What is KYC (Know Your Customer)?

KYC, short for Know Your Customer, is the required step banks and financial companies must take to check and confirm their clients’ identities. This requirement is set by the Financial Conduct Authority (FCA) to make sure customers are who they say they are. This process is key in anti-money laundering (AML) and is vital for keeping financial transactions honest and protecting against money laundering activities the UK.

What are KYC Checks?

Know Your Customer checks – often shortened to KYC checks – are a way for companies to assess and confirm a customer’s identity, their financial activities, and the risk they pose. The goal is to prevent fraud, money laundering, and other financial crimes by ensuring that customers are who they claim to be. If a customer fails to meet the minimum KYC requirements, a company or financial institution may refuse to do business together as it could open them up to the risk of fines, financial crimes, and reputational damage.

Last year, our Experian Fraud Index flagged significant growth across multiple types of fraud. Take financial crime attacks on current accounts, for example. These have shown to have increased significantly with up to 1% of new applicants identified as fraudulent. The financial crime landscape is ever evolving and tighter measures and regulations within anti-money laundering and KYC are needed to match this rate of change.

For individual customers the process typically involves providing proof of identity and address. For corporations, the checks are a little more complex and require details such as corporate registration and information on directors and beneficial owners. The checks can take place both in the first instance of working together and on an ongoing basis.

Who regulates KYC?

KYC regulatory frameworks exist worldwide and are mandated by each region’s financial regulatory authority. In the UK, it’s the Financial Conduct Authority (FCA) who set out KYC requirements under the Money Laundering Regulations. The aim of these is to establish formal customer identification programmes that also allow businesses to monitor customer transactions on an ongoing basis. Together, they help flag suspicious activity and crack down on crimes like money laundering.

How is KYC different from other checks?

KYC aren’t the only checks a business can put in place to protect itself. Both Anti-Money Laundering (AML) and Know Your Business (KYB) help to assess risk in relation to financial crime.

They all share an objective to ensure financial transactions are legitimate and safe, but there are a few key differences for KYC vs KYB vs AML:

![]()

KYC checks

focus on consumers and identifying a named individual, which could be an owner of a business.

![]()

KYB checks

focus on verifying businesses. As part of a KYB check, the owners and other key parties of the business also undergo a KYC check.

![]()

AML checks

help ensure that the business or consumer being onboarded by a financial provider is not involved in financial crime.

Who is subject to KYC regulations?

By creating a line of defence against financial crime, KYC regulations have significantly reshaped and protected the industries that are required to enforce them. These include:

- Accountants and tax advisers

- Banks, credit, and financial institutions

- Cryptoasset businesses

- Estate agents

- Gaming and casino businesses

- Legal professionals

- Luxury goods and art dealers

- Management consultants, auditors, and insolvency practitioners

- Trust providers

What is eKYC?

KYC verification involves checking a lot of information and documents, many of which can be complex. However, regions are turning to digital solutions in order to complete the process. This is known as Electronic Know Your Customer (eKYC).

Artificial intelligence (AI) has even started to play a part in eKYC, with machine learning helping to detect risk factors.

It’s important to remember that not all checks can be completed electronically – such as hard-to-change legacy requirements – and manual investigations will always have their place. However, for the most part eKYC offers a range of benefits such as:

Accuracy

Mistakes can slow a process down and be a drain on time, resources, and costs when working to put them right. However, digital systems help to eliminate the risk of human error, with eKYC automatically checking for mistakes and being able to put a quicker fix in place.

Adaptability

Regulations can often be subject to change, meaning compliance systems need to be updated, as well as employee training. eKYC systems can implement those changes in a faster, scalable way that doesn’t interrupt workflow.

Cost

eKYC systems come with a price tag, but they can help to save money in the long run thanks to improved accuracy, faster processing speeds, and better utilisation of resources. They also help to free up employees’ time which can be spent on other tasks or areas of the business.

Speed and ease

A study by Deloitte found that 38% of new banking customers[1] will abandon the account creation process if they feel that onboarding is taking too long. eKYC eliminates the need for paper documents and IDs, offering a smoother and more convenient customer experience.

A large UK bank found a ~70% reduction in manual checks for consumer customers using Experian automated KYC solutions.

What are the benefits of KYC checks?

Risk mitigation

KYC checks allow you to assess and manage the risks associated with your customers, reducing the likelihood of criminal activities. This will support financial loss prevention for you and your customers and help keep laundered money out of the financial system.

Financial crime prevention

Financial crime is said to cost the UK economy around £290 billion annually. From terrorist financing and money laundering to identity theft, fulfilling your due diligence through KYC compliance means you can help put a stop to illegal financial activities.

Regulation compliance

Regulated businesses must comply with various requirements to prevent money laundering and other financial crimes. KYC checks help ensure adherence to these regulations, avoiding legal repercussions and damage to brand reputation. Failure to meet KYC compliance can also lead to hefty fines and even criminal convictions. In just the second half of 2022 HM Revenue and Customers (HMRC) fined businesses a total of £3.4m[2] (£3.2 for named businesses, £200,000 cumulative smaller fines) for breaching anti-money laundering regulations. In the US, regulators issued individual organisations fines of up to $4.3b[3] in 2023.

Cost savings

Identifying and preventing criminal activities early on helps in minimising financial losses, saving resources that would otherwise be spent on investigating and rectifying fraud or AML-related issues.

Enhanced customer trust and experience

By demonstrating a commitment to security, you can build trust with your customers. Transparent KYC processes reassure customers that their financial transactions are secure. Using multiple data source verification, advanced analytics, and automation, the KYC process can be streamlined to improve customer experience.

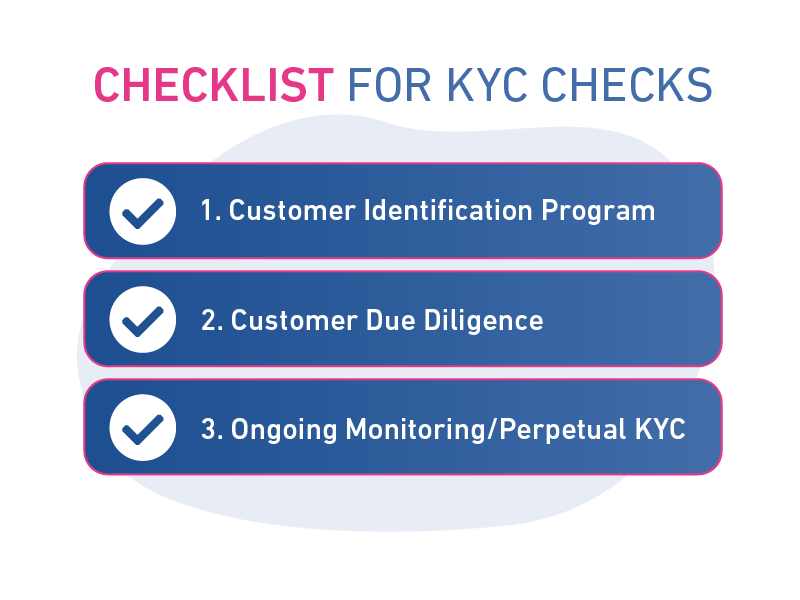

Checklist: How do I undertake KYC checks?

KYC checks are split into three components – sometimes referred to as pillars – which help to firstly verify and ensure due diligence, then determine risk profiles, and finally to practise ongoing monitoring.

It’s important to remember that KYC checks are not a one-time event. Customer activity and risk profiles can change over time, so you should be prepared to undertake periodic due diligence and monitoring. Similarly, records for such due diligence should be kept for both internal and regulatory purposes.

1. Customer Identification Program

The first step in your KYC process will be the Customer Identification Program (CIP) to establish that a customer is who they claim to be. This is the step which requires you to obtain and verify documents such as government-issued IDs and addresses for clients, or Ultimate Beneficial Owner (UBO) details and financial statements if they’re a business.

As well as proper collection and use of this data, the CIP should be completed in a timely manner and documented.

2. Customer Due Diligence

Customer Due Diligence comes next, taking verification further by seeking confirmation from banks and financial institutions that the customer in question can be trusted.

This part of the process is about establishing risk, and can be further split into three levels:

![]()

Basic Due Diligence

This is carried out for all customers and involves gathering additional information, such as the location of the customer and the types and patterns of their financial transactions. For corporate customers, this basic due diligence needs to be carried out for anyone identified as a UBO.

![]()

Simplified Due Diligence

For those considered low risk clients, Simplified Due Diligence can be used. This is a more straightforward and streamlined approach to the checks.

![]()

Enhanced Due Diligence

If a client appears to be a higher risk, more information and additional checks with agencies and public sources will be needed.

3. Ongoing Monitoring / Perpetual KYC

Ongoing KYC checks and monitoring, sometimes known as perpetual KYC (pKYC), will help identify suspicious changes to behaviours or activities that may change a customer’s risk profile. An established process should be put into place for ongoing monitoring, and this should look at:

- Adverse media coverage of the client

- Changes to customer or transaction locations

- Changes to customer transaction types, frequency, or amounts

- Inclusion on the Politically Exposed Persons or a sanction list

Ways to conduct KYC checks

What is it? | When is it used? | |

Bank account verification | Verifying the ownership of a bank account by using verified third-party data from the issuing bank. | Bank account verification is typically used during the onboarding process, when a customer establishes a new relationship with a financial institution. It can also be employed if amending existing details that will include the use of a Direct Debit or Direct Credit facility.This type of verification can supplement other KYC solutions to increase the trust with regard to the application or transaction. |

Biometric verification | Using biometric data, such as fingerprints, facial recognition, or iris scans to authenticate the identity of customers. | Biometric verification can be implemented during account opening, account login, transaction approvals, or any other critical points in the customer journey. |

Digital identity verification | Using advanced technologies to verify digital identities through a combination of behavioural analytics, device fingerprinting, and geolocation data. | Digital identity verification is often employed in real-time during online transactions and can provide an extra layer of security. |

Document verification | Verifying the identity of customers through official documents such as government-issued IDs, passports, and utility bills. | Document verification is typically employed during the onboarding process, when a customer establishes a new relationship with a financial institution. |

eKYC validation | As outlined above, eKYC validation involves verifying the existence of an identity through the use of verified third-party data assets. This includes existing financial agreements, voters’ registration and deceased registers. | eKYC validation is considered a frictionless method that is typically employed during the onboarding process. For example, when a customer establishes a new relationship with a financial institution. |

Ongoing monitoring | Continuously monitoring customer transactions and behaviour to detect any anomalies or suspicious activities. | Ongoing monitoring is essential for identifying changes in customer behaviour or circumstances that may signal potential suspicious activities. |

Remediation | One-off or periodic reviews of a segment of your portfolio to check for changes in circumstances and risk or inconsistencies in data.The objective here is to update and verify the data you hold for a customer. | Periodic remediation is needed on a fairly regular basis – usually 1, 3 or 5 years, depending on the risk profile. This is to appropriately verify a customer’s identity and monitor for changes which could impact their profile. |

What is a KYC document?

A KYC document is a document used to verify a customer’s identity and personal details.

Below are the KYC documents that are mandatory within the UK, segmented by client and company type.

For UK banks and financial institutions:

- Proof of identity, such as a passport, driver’s licence, or other form of government-issued ID

- Proof of address, such as a utility, rent, phone, or tax bill, or a mortgage statement

- Proof of income, such as a tax return, tax statement, letter from employer, or recent bank statement

For individual and corporate clients:

- Full name

- Date of birth

- Residential address

- Proof of identity, such as a passport, driver’s licence, or other form of government-issued ID

- A second supporting document issued by a public sector body, judicial or government authority, or other FCA-regulated entity in the UK

According to the FCA, proof of identity can be in both document and digital form.

For UK Companies:

- Full name

- Registration number

- Government-issued ID

You will also need to verify the company by confirming its listing on a regulated market, undertaking a search in the relevant company registry, or by obtaining a copy of the company’s Certificate of Incorporation.

For private and unlisted companies, the above is required as well as some additional information:

- Names of all directors

- Names of the Ultimate Business Owner (UBO)

- Names of related individuals who have control over the company

How we can help

Our range of automated KYC solutions have resulted in:

- ~70% reduction in manual checks for consumer customers

- ~40% reduction in manual checks for commercial customers

Potential cost saving of over 50% for a large UK retail bank having tamed an unruly remediation backlog.

Implementing KYC processes and conducting necessary checks can be resource-intensive. However, we can help you meet the appropriate requirements by carrying out initial KYC checks on your existing customers and providing flexible solutions with our data assets and analytics expertise.

Using our third-party data, we can help you automate your KYC checks and monitor your portfolio, as well as flagging when manual intervention may be needed – if a customer’s risk profile has changed, for example.

A multi-faceted approach that combines various verification methods and ongoing monitoring helps you stay ahead of emerging threats, strengthen your defences against financial crime, and build a secure, trustworthy financial ecosystem for your customers.

Find out more about how we can help you with your KYC checks.

[1] Improving the account opening process for Millennials and digital banking customers, Deloitte

[2] HMRC issues £3.2 million in money laundering penalties, GOV.UK

[3] Biggest AML Fines of 2023, Skillcast