Before Covid-19 hit, we were already seeing people being financially exposed, with an estimated 8.3 million consumers over-indebted. The scale of exposure has now been accelerated, with many consumers suffering income shock – and facing unemployment.

Recent research by YouGov found that 28% of the UK think that their financial situation has worsened since the pandemic hit and 67% think there will be a depression/recession in 12 months’ time. In these uncertain times, customers are looking to lenders and other providers for support and guidance.

Understanding what customers want is an integral measure to any strategy design. In this blog, we look at what customers want from providers which can provide you with insight for supporting them and building long-lasting, stronger relationships.

Customers expect advice and support

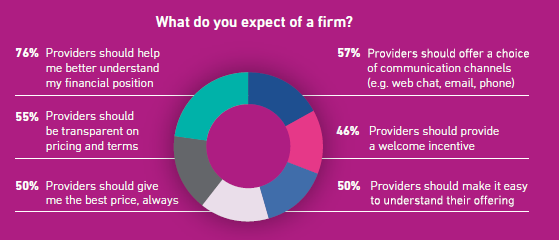

In the UK, consumers have a gap in their financial knowledge, with Experian research finding 80% admitting they find it hard to understand their financials using existing account management tools, but they are also willing to receive help. Almost 3 quarters (70%) of people want advice while applying online and those using mobile phone would like prompts to help them make better choices.

These findings show a real need for lenders to support customers further during the application process by providing further information and the ability to ask questions, e.g. Live Chat.

Enhancing consumers financial knowledge

One of the most valuable things you can do with a customer’s financial data is present it back to them. Most customers have large financial product portfolios and it’s hard to keep track of all of them. If you can access this information, you have an opportunity to present it back to them in an easily digestible way which would be hugely beneficial for consumers.

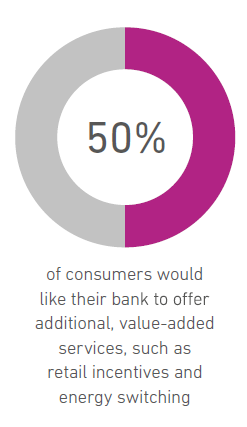

Our research demonstrates this need for advice and guidance with half of customers saying they would find it beneficial if their bank was to offer value-added services, such as retail incentives or energy switching. Customers also say they want advice across many other financial products such as current accounts, mortgages, life insurance and more.

Customers want fast, easy, friction-less experiences

In today’s digital world, it’s a must to provide your customers with streamlined and intuitive online experiences. 74% of consumers bank and buy online so removing any friction from your customer journey is clearly a priority for many businesses. This is evidenced as we asked businesses about what their priorities were and 74% said improving customer experience is a high priority.

!function(e,i,n,s){var t=”InfogramEmbeds”,d=e.getElementsByTagName(“script”)[0];if(window[t]&&window[t].initialized)window[t].process&&window[t].process();else if(!e.getElementById(n)){var o=e.createElement(“script”);o.async=1,o.id=n,o.src=”https://e.infogram.com/js/dist/embed-loader-min.js”,d.parentNode.insertBefore(o,d)}}(document,0,”infogram-async”);

67% of customers surveyed would like to know which financial products they are pre-approved for before they apply. Pre-approval saves them time, reduces anxiety in the application process and ensures their credit rating is never compromised due to a failed application. Further to this, 47% of customers would like the convenience of pre-populated details on application forms. Businesses need to gain an in-depth understanding of how your customers want to be interacted with and how these experiences can be delivered.

Through this insight, businesses can map out the current customer journey and identify points of friction and this needs to be considered across channels, not just digital. An example of a point of friction is the need to provide paper copies of information, such as utility bills or bank statements.

Deliver new valuable and trusted experiences

To help customers achieve their financial goals and support them through difficult times, you need the latest and most accurate data.

Personal Financial Management tools

Personal Financial Management (PFM) tools can provide customers with a clearer view across their financial product portfolios, so they can digest the information easier and have a single convenient place to refer to. This could also allow you to make suggestions or provide prompts on how users might want to alter their spending in order to achieve their financial goals, e.g. increase savings. Secondary to this, being able to help customers understand their finances and how it can be improved to meet their financial goals will help build trust and brand affinity which could improve loyalty and lifetime value.

Review and reshape your data strategy

With the right data collection, aggregation and analytics capabilities, you can make faster and more informed lending decisions which can position you as a trusted adviser for customers. If you’re seen to help customers to grow financially, you will be front of mind when they consider future financial decisions; building longer-lasting relationships which are profitable for both you and the customer.

Make life easier and more convenient for customers

Prepopulating data can allow you to be more certain about the accuracy of the information being provided while also saving the applicant time. Open Banking data could replace laborious and inconvenient tasks, such as providing paper copies of financial information, and allow you to access a customer’s income and outgoings in real-time. Furthermore, you can access signals from the data which can be modelled into triggers, allowing you to proactively offer support if financial stress is occurring, or prequalify for further products.

Risk based authentication

The authentication process is vital for businesses to prevent fraud but often is one of the biggest sources of friction in the customer journey. Risk based authentication can work seamlessly in the background by analysing digital data, such as device information, and behavioural biometrics to quickly authenticate the customer’s identity with confidence.

At Experian, we have the expertise and solutions to help you build trusted relationships with your customers and improve the customer experience. Reach out to your account manager or contact us to find out more.